Preparing for 2018

As something of a scary ‘sneak peak’, the Irish Brewers Association’s Jonathan McDade took seminar participants through the most likely consequences of the Government’s enacting The Public Health (Alcohol) Bill in its present format, labelling it nothing less than “a threat to prosperity”.

Ireland is the eighth-largest beer producer in the EU and exports €280 million-worth of it a year.

Alcohol abuse diminishing

Jonathan McDade told those attending that alcohol consumption has fallen 25% in Ireland since 2005 according to the World Health Organisation itself and an ESPAD survey found that underage drinking has come down by 48% in 20 years. Between 2015 and 2016 a Health Ireland survey found binge-drinking reducing by 7%.

Unintended consequences of Bill

Damage to product innovation and to trade with the EU number amongst the unintended consequences of the Alcohol Bill being introduced in its present format.

Recent indigenous entrants to the Irish market will have a harder job marketing their product and international investment will suffer, he said, adding that the Bill’s sponsorship restrictions mean an end to alcohol sponsorship of sporting or cultural events.

All this will adversely affect an industry employing 4,000 in the agricultural sector.

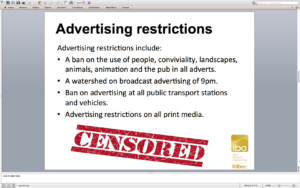

Advertising restrictions

The Bill proposes advertising restrictions that will ban the use of people, conviviality, landscapes, animals, animation and the pub itself in all adverts.

It will introduce a 9pm watershed on broadcast advertising and ban advertising at all public transport stations and on vehicles as well as imposing advertising restrictions on all print media.

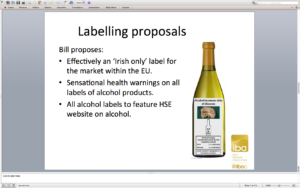

Labelling restrictions

Labelling restrictions to be introduced by the Bill would effectively require an ‘Irish only’ label for the EU market, said Jonathan McDade. It would also seek “sensational health warnings” on all alcohol product labels and all alcohol labels would have to feature the HSE’s alcohol website.

“And where is the evidence for introducing such restrictions?” he asked, pointing out that the much-vaunted Loi Évin in France had been a failure with binge-drinking and alcohol abuse on the rise there.

Nor had there been any solid information on the benefits of the specified labelling requirement proposals either.

The Health Department was meant to carry out a Regulatory Impact Assessment on its proposals. But its RIA remains unpublished and large sections of it – those contrary to the thrust of the HSE zealots – are missing, he claimed. Indeed, it would seem that no others were consulted in formulating the Department of Health’s RIA on industry and tourism.

“The only ‘academic research’ cited is that of the University of Sheffield report which has been widely discredited,” he said.

This Bill was passed by the Seanad at the end of December and is passing through the Dáil at present.

“If passed it will probably have a three-year transition into law,” he said.

The industry has lobbied intensively for amendments to this Bill with ABFI calling for meaningful engagement with the Department of Health and for balance in the Bill.

“We want recognition that we’ve a positive role to play to achieve the stated aim of tackling alcohol misuse,” he said in urging all present to meet with their TDs and Senators on the matter.

The past, present and future drivers of global alcoholic drinks

The IWSR’s James Fellowes highlighted the likely trends for 2018 at the seminar. The IWSR, the leader in global intelligence for trends in the marketing of alcohol beverages, covers markets in 156 countries.

He began by discussing the concept of total beverage alcohol.

By 2021 the global market for alcohol is forecast to grow by an additional 300,000 cases, he said, bringing annual consumption to 28 billion cases.

Spirits, which showed a CAGR of 0.6% between 2011 and 2016, would witness a slowing to 0.4% growth from 2016 to 2021, he said.

Wine, which showed 0.3% CAGR from 2011 to 2016, would show CAGR growth of 0.4% between 2016 and 2021 while beer would show CAGR of 0.1% from 2016 to 2021 having flatlined between 2011 and 2016.

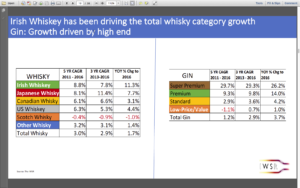

Irish Whiskey

Irish whiskey has been driving growth in the total whisky category with 11.3% year-on-year growth in 2016 (only Japanese whiskey, at 7.7% comes close in terms of degree of growth).

Jameson is still growing at around 10%. Tullamore Dew is growing at 7% and Bushmills sales are up 6%. Meanwhile Teeling sales are up 44% (albeit off a small base), he stated.

Future growth in the Irish whiskey market will primarily be in the US and Duty Free sectors along with Russia, Canada and South Africa. In the meantime, Malt whiskeys are looking at a projected growth of 15% (off a small base).

Irish whiskey has demonstrated a CAGR growth rate between 2013 and 2016 of 7.8% and a five-year growth between 2011 and 2016 of 8.8%.

Gin

Gin too has shown promise, with Super Premium varieties showing year-on-year growth of 26.2% while Premium grew 14.0% in 2016.

Super Premiums have shown a three-year (2013-2016) CAGR of 29.3% and a five-year CAGR (2011-2016) of 29.7% while Premiums showed a three-year CAGR of 9.8% and a five-year CAGR of 9.3%.

And brand dominance is also undergoing change. Value sales of Bombay Sapphire surpassed those of Gordons for the first time in 2016 as did Hendricks’ in surpassing Seagrams.

The largest gin markets are the UK, Spain, the US, South Africa, Duty Free, Germany, Uganda and Italy.

The UK, with sales of 1.4 million cases & Spain with sales of just over 1 million cases are driving this growth with the US – also now selling over one million cases – slowly catching up, according to IWSR.

In this rapidly developing gin category, with the market seemingly polarised between Premium and Standard gin, James advised that “Super Premium is where you want to be”.

So what will be the next ‘big trend’? The premiumisation of rum, he believes.

Beer & Cider

Beer is likely to remain in the sales doldrums globally with the fastest growth markets appearing to be Mexico, India and Vietnam.

But of the top 10 markets, seven are “going the wrong way” he stated.

‘International craft’ will drive beer value growth. The ‘megabreweries’ are particularly pertinent to this market as they buy up smaller craft breweries in order to access this market.

The fastest growth markets for cider from 2016 to 2017 have been South Africa, the UK and Canada.

“Cider growth is expected to slow across the globe and in all top 10 markets. New growth is expected from markets including Romania, Japan and Portugal.”

6 landscape-changing trends to watch out for

- Value divergence – the market is polarising into Super Premium & Mainstream according to IWSR. Consumers are trading-up and have increased product knowledge concomitant with the rise of professional bartenders. The Mainstream segment is growing well in many parts of the world thanks to the growth of the middle classes in major developing regions such as Africa and Asia where massive trading-up is going on in the former from sorghum to Heineken, for example. Alongside this there’s been an expansion of the hard-discount retailers (Walmart in US/Aldi & Lidl in UK). Also, with value divergence, the marketing hype no longer resonates with today’s younger consumer. Globally, Premium-plus spirits look set to see CAGR of 5.5% from 2016 to 2021 while Premium spirits are forecast to grow by 28% during this time so that by 2021 the global Premium spirits market is forecast to grow by 50 million cases, bringing annual consumption to 204 million cases. During this five-year period Super-Premium is forecast to grow by 39.6%.But Standard is also an attractive proposition for the consumer.

- Category blur – younger consumers “don’t give a damn about categories” and so category blur is happening speedily with some brands trying to keep up proving that an obfuscation of the beer, spirits and wine categories is taking place.

- Wellness – this is becoming a “monster trend” for drink (after food) and a key battleground for winning the quest for global betterment. From gluten-free to low-carb and wellness cocktails, under-indulgence has become sexy with phenomena like ‘dry January’ catching on. Globally, non-alcoholic bars and the concept of teetotalism are on the rise. “Non-alcoholism is the new vegetarianism,” says Richard Woods, the award–winning head of spirits and cocktail development at London’s Duck and Waffle.

- New premise – these ‘new premises’ use non-traditional selling channels – festivals, street fairs etc. Here, outdoor fairs and festivals give consumers the opportunity to “really engage” with alcoholic drinks brands. Today’s younger consumer is ‘highly experiential’. There’s also the development of the ‘Tap Room’ phenomenon in the US (filling 1,600 to 2,000 car park spaces) for the producer going direct to the consumer. Avoiding the traditional Route To Market and going direct to the consumer instead gives the producer 100% control over sales – and margins are therefore understandably ”off-the-roof”. This RTM also helps the producer enhance brand immersion.

- Flavours 2.0 – more sophisticated flavours are now being introduced including spice so that traditional spirits are being flavoured with sweeter, more familiar ingredients. This has attracted a new demographic and instilled new life across a range of categories traditionally seen to have a more challenging flavour profile such as whisky. So what started with the mega success of Fireball, for example, soon developed into a subcategory in its own right. In addition to the (more palatable) ‘cinnamon & spice’ brands, a number of niche – almost impossibly fiery – products are available today. ‘Dark flavours’, whether smoke, charcoal or new-style coffee, have also been embraced with consumers exploring more mature, less accessible flavours which add richness and character to the drinking experience. James pointed out, for example, that Peated Scotch, which is not new, is also on the rise as consumers demand more depth of flavour. Also oncoming is the phenomenon of ‘Bright Aperitifs’ made from striking colours that turn heads in the on-trade – and on Instagram. “Aperol was a game-changer that took the markets by storm thanks to its flavour and novel appearance,” he said, “Bright new drinks are now adding diversity to this trend.”

- Digitisation – James illustrated the changing face of convenience by referencing the progress of retail over the last 10 years as it changed from bricks & mortar shops to search engines five years ago. Now, the ‘e-premise’ is creating a new world order – and introducing ‘smart alcohol’ where the industry is transforming as ‘the internet of things’ revolutionises everything from packaging to how we order drinks.

Online sales in the US: Top 10 Brands

Bud Light

Tito’s Vodka

Corona Extra

Bulleit Bourbon

Coors Light

Stella Artois

Álamos Wine

Svedka Vodka

Absolut Vodka

Grey Goose Vodka