Hotel trading performance remains strong, deal flow subdued but gathering pace

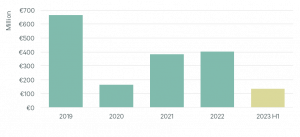

A total of €91 million worth of Irish hotel transactions were completed in Q2

Transactional activity in the hotel sector picked up in the second quarter of the year following a slow Q1.

This is according to CBRE Ireland’s ‘Irish Hotel Market Q2 2023’ publication, which details the transactional activity and trading performance in Irish hotels this year.

A total of €91 million worth of Irish hotel transactions completed in Q2, across six separate deals. A total of €135 million of capital was deployed on Irish hotels in H1 2023.

Hotel transaction volumes 2019-2023 H1

One of the most notable deals of the year was the sale of the Imperial Hotel & Spa in Cork city. The hotel is one of the most famous in the country and a place of historical significance for both Cork and Ireland. A private Irish hotel operator acquired the hotel for approximately €25 million.

Development activity remains quite robust, despite escalating build costs and debt challenges. A recent notable transaction was the sale of Telephone House, an office building in Dublin 1, to JMK Group, which will be converted to a 296-bedroom aparthotel. This trend of offices being considered for hotel conversion is an emerging one.

Private investors, family offices and hotel groups have dominated transactional activity in the Irish market this year, with institutional investors and private equity groups less active. This has the potential to change late in the second half of the year, should these investors get more comfortable with asset pricing and the cost of debt.

Occupancy rates across all Irish cities, including Dublin, remain strong. On a year-to-date basis (to the end of May), occupancy in Dublin has averaged 78%, relatively in line with levels achieved for the same period pre-pandemic in 2019. A busy summer period will see this rate continue to grow. Average daily rates (ADR) have also continued to increase sharply.

Indeed, the month of May saw a record-breaking ADR of €209 achieved in the city, 3.5% ahead of the previous monthly record, achieved in September 2022. On a year-to-date basis the ADR across all stock in Dublin is approximately €170. While top-line performance has been strong, hotel operators are still experiencing increased operational costs due to higher wages, utilities, and F&B expenses and this is impacting bottom-line performance.

“Deal flow picked up pace in the Irish hotel market in Q2 and we saw a total of €91 million of transactions close,” said director and head of research at CBRE Ireland, Colin Richardson. “Private investors and family offices are particularly active in the current market. The hotel sector remains attractive to institutional investors and lenders given the strong trading performance of both Dublin and regional hotels.”

Executive director and head of hotels at CBRE Ireland, Paul Collins said: “we continue to see strong appetite from a variety of prospective purchases for hotel opportunities in Ireland, including trading assets, investments, and development sites. We expect transactional activity will continue to pick up as the year progresses.”