‘Food-led’ pubs replacing ‘locals’ in UK

In the UK, pub operating costs take up 48.7% of total turnover in the average freehold premises. So finds market researcher CGA Peach/CGA Strategy in a new report commissioned by he Association of Licensed Multiple Retailers there.

Future Shock, the first issue of which was published recently, finds that payroll costs have risen from 24.2% of turnover to 26.4%, with operational costs linked to legislation and regulation accounting for 5.7% of total turnover.

But it’s food which has come to figure very highly in the on-trade mix.

Food figures

According to the ALMR, “Our Benchmarking Report this year shows town centre food-led businesses have replaced the community local as the average on-trade outlet”.

With food-led outlets accounting for over one-third of all outlets and with wet sales accounting for 65% of turnover across all sectors, the ALMR report takes a closer look at certain target markets, profiling customers from a number of differing age brackets and relating them to segment preference and likely socio-economic values within this sector.

18-24 year-olds with No Children

How often do they go out?

Future Shock finds that the typical pre-family under-25 consumer goes out to drink once a week, but they’ll go out five to six times a month to eat – and venues can include both non-licensed and licensed.

The report points out that despite commonly–held preconceptions, fewer than half this segment claims to go out to drink ‘at least weekly’. Less than one in 10 go out drinking three or more times a week.

“A bigger proportion, around one in seven, claims not to have gone out to drink at all in the last six months.

“Meanwhile, 50% of these pre-family young adults eat out at least once a week and less than 5% say they didn’t eat out at all in the previous six months.”

What affects their going out frequency?

The report finds that four in 10 of all 18 to 24 year-old pre-family consumers drink out at least weekly. And there’s a noticeable difference between those still living with parents (36% of whom go out to drink weekly or more often) and those living in rented or owned accommodation where the proportion rises to 45%.

Around 70% of those who drink out weekly also eat out at least that often.

What’s important to them?

The most-mentioned factors affecting eating out choice at lunch, for example, are the quality of the food and coffee closely followed by service. In the early evening, food choice, previous experience, environment and convenience are the most mentioned factors.

Mythbusting

To belie media stereotypes, soft drinks form the largest product category among pre-family 18-24s. 64% of them drink these when in pubs, bars or restaurants, well ahead of the second-most popular category, cocktails (consumed by 43%).

“Coffee is the fifth most commonly consumed drink out-of-home by these consumers – three times as many drink it compared to the numbers who drink alcopops,” states Future Shock.

“Lager, so often the media’s prime suspect, is drunk out-of-home by only one in three of these consumers.

“The drinks these consumers are disproportionately inclined to buy out-of-home compared to other drinkers are the ‘younger’ spirits such as Tequila, vodka and liqueurs, cocktails and ‘alcopops’. But the penetration rate of soft drinks in this group is also around 30% higher than among all out-of-home drinkers.”

Non-traditional consumption

Not surprisingly, young adults consume in non-traditional ways.

With wine, for example, they’re much less likely to have a favourite country of origin, varietal or wine brand.

“Their lager-drinking shows a clear skew towards bottled and craft lagers rather than draught standard/premium variants – and their level of engagement with the category is revealed by the fact that they’re noticeably more concerned about the range of lagers stocked than out-of-home drinkers overall (38% of 18-24s said that range of lager was extremely important compared to 26% of all out-of-home drinkers).

“Their cider-drinking is also non-traditionally biased – in favour of fruit ciders and in favour of bottled served over ice rather than draught (58% of 18-24s said they prefer cider served over ice from a bottle compared to 40% of all out-of-home drinkers).

The report advises that this market segment is “fertile ground for brand owners and retailers because they are – perhaps not surprisingly – more disposed than average to consider and to try new drinks and brands when out drinking. But with income levels a little below the average, their willingness to experiment and to socialise is a little constrained and their sensitivity to deals is therefore probably heightened.”

25-44 year-olds with Children Up To the Age of 16

Market significance

Future Shock reports that, “25-44 year olds with children not only eat out more frequently than average, but they also drink out more often. Over half of them eat out at least weekly and over 40% of them drink out-of-home weekly. Nearly one in four eats out and one in five drinks out at least three times a week”.

Often seen as a barometer of consumer and economic vitality, this represents a key target audience for many players in the out-of-home food market, states the report, adding that it’s one of the most competitively intense market segments in the business.

This consumer cohort accounts for around one in six of the adults surveyed in CGA Peach’s Brand Track research but the evidence remains clear that this segment is disproportionately important to the out-of-home market and therefore the licensed trade market, accounting for almost 30% of it.

What do they drink out of home?

Lager, soft drinks and wine are the drinks categories consumed when out drinking by most in this segment, followed by coffee and cider.

“Being under the age of 45, the dominance of lager in the beer repertoire is very clear: 48% of this market drinks lager out-of-home whilst only 15% of them drink ale. Twice as many in this segment drink cider out-of-home compared to the number of ale drinkers – and more people in this market claim to drink craft beer than to drink ale.

“The majority of lager drinkers in this market segment are draught premium or standard lager drinkers – with marginally more claiming to drink premium than standard. But compare their profile of consumption with the total out-of-home market and their skew towards speciality/craft lagers is clear.”

This market segment also remains more likely than the population overall to try new or different drinks when out-of-home with one in four stating they often like to do so compared to only one in seven for all out-of-home drinkers.

The 55+ market

How often do they go out and what affects them?

The report finds that a fairly large proportion (32%) of this group had not been out to drink in the last six moths before interview compared to 21% for the population overall.

Where and when do they eat and drink out?

Almost two-thirds of this segment say that alcohol’s not at all important when making choices about where to eat out.

What do they drink out-of -home?

The overwhelming importance of wine to this segment is clear. It’s drunk by over half of those interviewed, well ahead of any other alcoholic category.

“Lager is the second most widely-drunk alcoholic category in this population, consumed by 30%,” states the report. Meanwhile, all the spirits categories under-trade with this audience are consumed by less than one in 10 of the 55+ market.

“One in four of this segment drinks ale out-of-home, a higher penetration than for the out-of-home drinking population as a whole (at one in five).”

This segment is less predisposed to try different or new drinks when out drinking, but this is certainly not a closed door,” notes the report, “Only one in three of this demographic group says they never like to try new drinks and this group is likely to be older, with lower incomes, retired and with less frequent drinking-out patterns”.

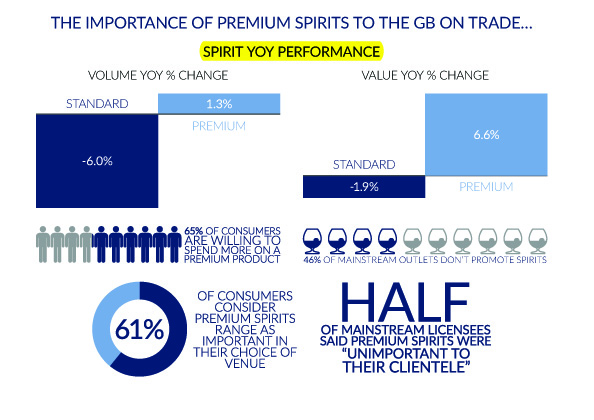

The importance of premium spirits to the GB on-trade

While the volume of ‘standard’ spirits declined 6% with a concomitant decline in value of 1.9% at a time when premium spirit volumes rose by 1.3% and premium spirit values increased by 6.6%, states one of the report’s sponsors, Pernod Ricard.

The French company found that 65% of consumers are willing to spend more on a premium product yet 46% of mainstream outlets in the UK don’t promote spirits.

Half of mainstream licensees said premium spirits were “unimportant to their clientele”. This seems strange since Pernod’s research also found that 61% of consumers consider the premium spirits range as important in their choice of venue.

Future Shock Issue One: ALMR uses research from CGA Peach and CGA Strategy. The report was partnered by Sky, Heineken and Pernod Ricard.