Have we become a nation of wine lovers?

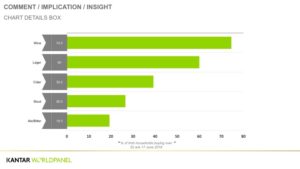

While the perception of Irish alcohol drinkers elsewhere in Europe is more often than not linked to beer and stout, the stereotype doesn’t necessarily hold true when considering grocery purchasing of alcohol. Almost three-quarters of Irish households (75%) bought at least one type of red, white or rosé wine over the last 12 months, meaning its overall popularity is greater than that of lager (60%), cider (39%), stout (27%) and ale/bitter (19%).

Furthermore, the drink’s popularity shows no sign of waning either; value sales grew by 7.3% to €474 million this year with the average shopper putting at least one bottle of wine in their basket between two to three times a month. That’s twice as much compared to the same period a year ago, with lower prices likely encouraging shoppers to engage with the category more frequently – the average price paid in the last year has fallen by 2%.

Wine shoppers

Irish wine shoppers fall into three distinct groups: those that only buy red (18% of shoppers), those that only buy white (21%) and those that buy a combination of both (42%).

The group that buys both throughout the course of the year are more affluent and more valuable to the category as they engage more frequently and are key to the overall health of the wine category.

Age is a more obvious differentiator with the majority of spend on red wines coming from older shoppers – 61% of spend comes from those aged over 45. In white wines, the share of spend from those aged 45 or over drops to 46%.

In sales terms however, red wine is the clear winner with Irish households spending €246.3 million in the last year, up 8% on last year. While white is growing at the same rate, up 8%, overall sales were slightly lower at €215.6 million. In both cases increased frequency of purchase has been the primary driver of growth. However, it’s also worth noting that individually both red and white wine are attracting new shoppers ie shoppers who normally buy red wine adding white to their repertoire and vice versa, boding well for the longer-term growth of both.

Chilean goes from strength to strength

Chilean wine now accounts for more than a quarter of all take-home wine sold in Ireland following another year of impressive double-digit growth. Of the Old World wines, Spanish (14%), French (13%) and Italian (10%) are the most popular with Irish shoppers while Australian (16%), South African (7%) and New Zealand (5%) are the most popular of the new world wines.

Age is a more obvious differentiator with the majority of spend on red wines coming from older shoppers.

Although cider benefits from hot weather, lager remains number one in LAD

Irish households spent an impressive €226 million on lager alone in the latest year, with six in every 10 Irish households buying into the category, cementing its position as Ireland’s go-to choice within take-home LADs.

While value sales of lager were down slightly on last year by 0.1%, Irish households actually increased the quantity they purchased with overall volume sales up 8%. This was, however, offset by a decline in the average price shoppers paid – prices fell by 8% over the last year – effectively meaning shoppers got more bang for their buck when buying lager.

Meanwhile, cider continues to go from strength to strength with the category continuing to attract more shoppers for the second consecutive year.

The cider category has unquestionably been boosted by the recent warm weather. Comparing the 12 weeks to 17th June with the same period last year, cider sales saw double-digit growth. Over the longer term, growth is slower but still robust. Irish shoppers spent just under €59.8 million on cider in the last year, up 5% on the €56.7 million spent in the previous year. As with lager, growth in the cider category was predominantly volume driven, with prices falling by 2% over the last 12 months.

Overall volumes sold were up 7%, driven by two key drivers – more shoppers and increased engagement from existing shoppers.

A significant 39% of Irish households bought into the cider category this year, up from 37% of households in 2016 with that increase in penetration alone generating an additional €1.2 million in sales.

The other key contributor to growth came from existing cider shoppers buying into the category more frequently. The average shopper bought into cider between nine and 10 times throughout the year, up 3% on last year, generating a further €1.6 million in sales.

For the second consecutive year the ale/bitter category has recorded robust double-digit growth with value sales up 12% overall to €35 million, the only one of the categories to see prices rising, up 4% on last year. One in five households bought into the category over the latest 12 months, but with overall penetration at 19.3% there’s still substantial room for growth when benchmarked against lager (60%), cider (39%) and stout (27%).

Half of shoppers are loyal to one type of LAD while the other half spread their spend across two or more types

Although a substantial proportion of Irish households are solus shoppers ie they’re loyal to just one type of drink – lager, cider, stout or bitter/ale – the majority of shoppers (53%) buy into a combination of drink types over the course of a year.

As expected, lager attracts the greatest proportion of shoppers that buy only lager and nothing else (29%). However cider also attracts a substantial group of solus shoppers – 11% of Irish households buy cider exclusively while stout and ale/bitter shoppers are more likely to buy one of the other types of drink in addition to stout or ale/bitter.

When considering each of the lager, cider and stout categories the shopper profile becomes progressively older and less affluent from lager, to cider to stout.

As expected, stout attracts the oldest shopper with 78% of spend in stout coming from shoppers aged 45 or over. Cider shoppers are younger with 64% of spend coming from shoppers over 45 while lager attracts the youngest of the three – 56% of spend attributed to shoppers aged over 45.

The level of affluence is another key differentiator across the three types. While 40% of spend on lager comes from the more affluent ABC1 group, this falls to 36% and 23% for the cider and stout categories respectively.

An eye on next year and MUP

With an eye to next year and the potential introduction of Minimum Unit Pricing in Ireland, we can expect to see a certain level of price inflation should legislation be introduced. This is likely to have an impact on brands or segments within categories as shoppers either change their purchasing behaviour between brands within a segment or go from one segment/category to another segment/category.